Why buy your first home when you can build it? The Australian Bureau of Statistics (ABS) shows that In August 2016 alone 5,641 new construction mortgages were opened, so Australia clearly loves to get creative with its new homes. You'll have total control over the final shape of your home, gain the ability to add value through smart design and a slow start to paying off your loan with a construction mortgage.

But on the flipside you'll be totally responsible for your property's construction and mistakes could be costly. We've taken a closer look at building your first home to bring you a basic cost breakdown of the process.

Building your own home means that you can customise it however you'd like.

Building your own home means that you can customise it however you'd like.What will building cost me overall?

The Australian Architecture Association guide to preparing a budget estimated the total costs of building a home:

- $900 to $1500 / sqm for a Project home.

- $2500 to $4000 / sqm Architect designed homes and renovations.

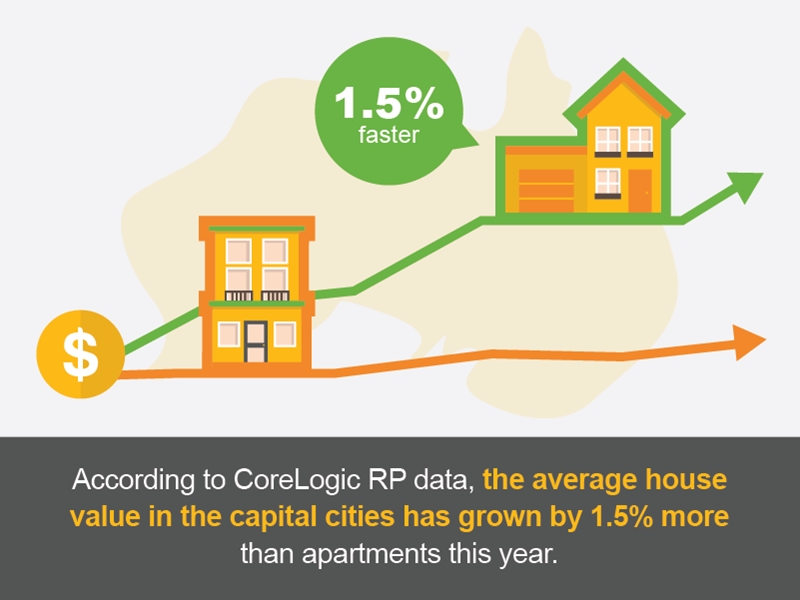

- The most recent data from the Australian Bureau of Statistics puts the average total cost of building a new home at almost $250,000.

If your home needs extra design or building work due to unexpected issues it will most likely be charged at the upper end of the rate scale so your projects costs could quickly balloon. A construction mortgage from Mortgageport can make managing and monitoring these unexpected costs easier than with a regular mortgage.

What will each step of building cost me?

Architects and design

AAA estimates the cost of home design at between 8 and 18 percent of the total construction cost. This amounts to between $136 and $306 per square metre. Using ABS data for the average floor area of a new home this will cost you between $34,000 and $75,000.

Materials

This cost will differ according to what kind of home you build. An Archicentre Cost Guide estimates that this will amount to roughly 46 per cent of total costs or $115,000.

Labour

A construction loan is very different from a normal first home loan.

This too can vary wildly according to the type of home you're building. Get quotes from several registered builders to make sure you're getting the best deal possible.

To give you an idea of the rough cost Archicentre estimates this will set you back you roughly 33 per cent of the total, or $82,500.

Fees, levies, permits and taxes

Archicentre states that fees, levies, permits and taxes will account for roughly 21 per cent of the total cost or $52,500. This varies from state to state and depending on your home.

Being able to release funds as you need them with your construction mortgage will ensure that you are able to afford these charges as they arise.

What exactly is a construction loan?

A construction loan is very different from a normal first home loan. The Australian Securities and Investments Commission's MoneySmart site explains that with this type of loan you withdraw money as you need it to pay tradespeople, until your home's completion when you revert back to a normal home loan.

There's a lot of work involved in building your first home.

There's a lot of work involved in building your first home.This is great for first time buyers, as you'll only pay interest on what you have borrowed – you'll only pay the full amount once the property is finished and you're living in it.

It's easy to get help

You wouldn't build your home without professional help would you? You shouldn't find a loan without the same level of assistance. A mortgage broker can act as the go between negotiating with your bank on your behalf if you have any issues.

The right broker may also be able to get you a better deal on your first home loan. Half a percentage less interest on a 30 year loan at ABS's median property price could save you well over $50,000 in interest payments over a 30 year term – that's nothing to scoff at.

You've got to think about sorting your first home loan before you even consider decorating!

You've got to think about sorting your first home loan before you even consider decorating!

Repaying your mortgage the right way could be the key to being happy in your home.

Repaying your mortgage the right way could be the key to being happy in your home.

A proficient architect will make sure that you get what you want out of a home.

A proficient architect will make sure that you get what you want out of a home.